Bartik Instrument

Shift-share IV in trade economics

August 26, 2025

Gains exist, distribution is messy

- Aggregate gains from trade are robust across HO, Ricardian, and new-trade models.

- Who gains and loses depends on factor mobility.

- HO: gains accrue to the abundant factor (Stolper-Samuelson), assuming factors move freely across industries.

- SFM (Specific Factor Model): in the short run, some factors are tied to a sector → clear winners and losers.

The textbook distinction in one line

- HO: long run, perfect mobility, factor-price equalization.

- SFM: short run, sector-specific factors, sectoral wage gaps.

- Empirical reality: the “short run” can last a decade or more, and the location of immobile factors is regional.

- This is what shift-share designs let us see in the data.

The within-country problem

- Cross-country evidence on gains from trade is settled.

- Within-country evidence is mixed and politically explosive.

- Why? Adjustment is spatial: districts, commuting zones, and provinces specialize in different sectors and absorb shocks differently.

- Reasons for imperfect mobility:

- skill mismatch (sector-specific human capital)

- geographic immobility (housing, family ties, language)

- institutional frictions (labor laws, licensing)

What we want to estimate

We want a local causal effect of a trade shock:

Yℓ=α+δXℓ+εℓ

- Yℓ — outcome in region ℓ (employment, wages, poverty)

- Xℓ — local exposure to the trade shock (e.g., change in import penetration)

- δ — the parameter we care about

Problem. Xℓ is endogenous: regions that import more are also regions where productivity, demand, or politics differ in unobserved ways.

→ We need an instrument for Xℓ.

The Bartik (shift-share) idea

Two ingredients:

- Shares sℓk — region ℓ’s pre-period exposure to sector k (employment, output, or expenditure share)

- Shifts gk — a common (national or world) shock to sector k

Combine into a single regional exposure measure:

Zℓ=∑ksℓkgk

The instrument predicts how hard region ℓ should be hit by a common shock, given its industrial structure.

Why call it “Bartik”?

- Tim Bartik (1991) used national industry growth rates interacted with local industry mix to predict local labor demand growth.

- The construct predates him (Perloff 1957, Freeman 1980) but the name stuck after Blanchard & Katz (1992) popularized it.

- In trade: replace national growth with tariff changes (Topalova) or import surges (ADH).

- Goldsmith-Pinkham, Sorkin, and Swift (2020) formalize it as a GMM problem with the shares as instruments.

A first numerical look

3 regions × 2 sectors. Tariffs fall between 1987 and 1988.

| region | LAgri | LManuf | sAgri | sManuf |

|---|---|---|---|---|

| A | 100 | 9 000 | 0.011 | 0.989 |

| B | 1 000 | 400 | 0.714 | 0.286 |

| C | 700 | 3 000 | 0.189 | 0.811 |

National tariff change 1987→1988: Agri 30 → 10, Manuf 20 → 5.

Bartik exposure Zℓ=sℓ,AgriΔlogtAgri+sℓ,ManufΔlogtManuf:

| region | Zℓ (Δlog) | Zℓ (Δlevel) |

|---|---|---|

| A | −1.38 | −15.1 |

| B | −1.18 | −18.6 |

| C | −1.33 | −15.9 |

Note the ranking flips: log change makes A most exposed; level change makes B most exposed.

What just happened?

- Manuf had the larger proportional cut: log(5/20)=−1.39 vs. log(10/30)=−1.10.

- Agri had the larger absolute cut: −20 pp vs. −15 pp.

- Which one matters? Depends on the outcome model: log-log specifications need Δlogt, level specifications need Δt.

- Lesson: the Bartik is only as well-motivated as the production-side or trade-elasticity model behind it.

First stage, reduced form, IV

The Bartik is used as an instrument:

First stage Xℓ=π0+π1Zℓ+uℓ

Reduced form Yℓ=ρ0+ρ1Zℓ+vℓ

2SLS ˆδIV=ρ1/π1

- Many papers (ADH 2013, Topalova) report the reduced-form coefficient ρ1 directly, calling Zℓ “exposure.”

- The 2SLS scaling requires π1≠0 and the exclusion restriction E[Zℓεℓ]=0.

Identification: two camps

Goldsmith-Pinkham, Sorkin, and Swift (2020) ask the central question: which assumption makes the Bartik valid?

| Camp | Source of identification | Champion paper |

|---|---|---|

| Share-based | Shares sℓk are exogenous to unobservables | Goldsmith-Pinkham, Sorkin & Swift (2020) |

| Shock-based | Shifts gk are quasi-randomly assigned | Borusyak, Hull & Jaravel (2022) |

Both deliver consistent IV under different conditions. The right diagnostic depends on which assumption you lean on.

Share exogeneity (GP framework)

Goldsmith-Pinkham, Sorkin, and Swift (2020) prove: the Bartik 2SLS estimator equals a GMM estimator where each share sℓk acts as a separate instrument, weighted by Rotemberg weights αk.

ˆδBartik=∑kαkˆδk

- ˆδk — just-identified IV using share s⋅k alone

- αk — Rotemberg weight, ∑kαk=1, can be negative

- A few industries usually carry most of the weight → the design hinges on the exogeneity of those few shares.

Rotemberg weights

For each industry k, the weight is

αk=gk⋅∑ℓsℓkXℓ∑k′gk′⋅∑ℓsℓk′Xℓ,∑kαk=1.

Two ingredients drive αk:

- size of the shift gk — industries with bigger national shocks matter more.

- first-stage covariance ∑ℓsℓkXℓ — how strongly industry k’s shares correlate with the endogenous regressor.

Weights can be negative: if gk and the first-stage covariance have opposite signs, that industry pulls the Bartik in the opposite direction. A handful of industries usually carry most of the weight.

Named for Julio Rotemberg (1983), who used the same decomposition logic in a different IV setting; Goldsmith-Pinkham, Sorkin, and Swift (2020) formalised it for the Bartik.

Rotemberg weights: 2x2

Use our toy data. Set Xℓ=Zlevℓ so the mechanics are visible: XA=−15.1,XB=−18.6,XC=−15.9, with shifts gAgri=−20,gManuf=−15.

First-stage covariances:

∑ℓsℓ,AgriXℓ=0.011(−15.1)+0.714(−18.6)+0.189(−15.9)=−16.45 ∑ℓsℓ,ManufXℓ=0.989(−15.1)+0.286(−18.6)+0.811(−15.9)=−33.15

Numerators: (−20)(−16.45)=329.0 and (−15)(−33.15)=497.2. Denominator 826.2.

αAgri=0.40,αManuf=0.60.

Manufacturing carries 60% of the Bartik. With 100+ industries in Topalova or ADH, 5–10 industries typically carry 80% of the weight — those are the shares whose exogeneity you actually need to defend.

Rotemberg weights in R

# shares: L × K matrix; g: length K; X: length L

fs_cov <- as.numeric(t(shares) %*% X) # first-stage covariances

alpha <- g * fs_cov

alpha <- alpha / sum(alpha) # Rotemberg weights

# per-industry just-identified IV

beta_k <- as.numeric(t(shares) %*% Y) / fs_cov

sum(alpha * beta_k) # = Bartik 2SLS estimateThe bartik.weight package (GitHub: paulgp/bartik-weight) does this and produces the Goldsmith-Pinkham, Sorkin, and Swift (2020) Table 5 diagnostic panel directly.

Diagnostics from Rotemberg weights

Goldsmith-Pinkham, Sorkin, and Swift (2020) recommend reporting:

- Concentration of weights — Herfindahl of |αk|. If 2–3 industries dominate, your identification is really about those industries.

- Top-5 industries — list them and ask: are their shares plausibly exogenous to local outcome trends?

- Pre-trend checks on Zℓ — does pre-shock Zℓ predict pre-shock changes in Yℓ?

- Just-identified IV by industry — if ˆδk varies wildly across top industries, the pooled estimate is fragile.

Shock exogeneity (BHJ framework)

Borusyak, Hull, and Jaravel (2022) take a different route. Treat the shifts gk as random and the shares as exposure weights.

- Identification: gk is uncorrelated with sector-average residuals.

- Works well when shifts come from outside the system you study (e.g., supply-driven Chinese import surge from China’s TFP and WTO accession).

- Diagnostic: tests for shock balance — does gk correlate with pre-shock industry characteristics?

- The ADH “instrument with other rich countries’ imports from China” exploits exactly this — it isolates the supply-driven component of the shock.

Inference: don’t use OLS standard errors

Adão, Kolesár, and Morales (2019) show that conventional cluster-robust SEs over-reject with shift-share regressors:

- Residuals are correlated across regions that share industry mix.

- Their fix: an exposure-robust SE that treats industries as the clusters of randomness.

- In R, you can implement AKM SEs via the

ShiftShareSEpackage or replicate by IV with industry-level data. - Rule of thumb for class: if you see Bartik with white SEs only, be skeptical.

Limitations to keep in mind

- Pre-period shares can be endogenous (industries locate for a reason).

- Common shocks may be heterogeneous across sub-periods → time-varying gk.

- Placebo tests on pre-period Y are essential.

- Weighting: by region size, by inverse SE, by employment — affects which observations drive the result.

- Aggregation matters: districts vs. provinces vs. commuting zones give different answers.

Topalova (2010): India 1991

- India’s 1991 liberalization cut tariffs unevenly across industries.

- Cross-district variation in pre-reform industry mix → cross-district variation in exposure.

- Difference-in-differences with Bartik exposure as the treatment.

Identification: the pace of tariff cuts was dictated by external (IMF) pressure and was negotiated industry-by-industry without regard to district outcomes → shocks plausibly exogenous to district trends.

Topalova: instrument

ZTopℓ=∑ks1987ℓkΔlog(Tariffk)

- s1987ℓk — district ℓ’s pre-reform employment share in industry k

- Δlog(Tariffk) — national log-change in industry k’s tariff between 1987 and 1997

Outcomes: district-level poverty headcount, poverty gap, consumption growth.

Topalova: specification

Topalova runs a panel across four NSS rounds (1983, 1987–88, 1993–94, 1999–2000):

Ydt=αd+γst+δTariffdt+W′dtλ+εdt

with district tariff constructed Bartik-style,

Tariffdt=∑ksdk,1987⋅Tariffkt

- αd — district FE (kill all time-invariant district traits)

- γst — state × year FE (absorb state-wide trends)

- shares frozen at 1987; national tariffs Tariffkt vary year-by-year

- IV: instrument realised tariffs with the scheduled tariff reduction path

Under two-way FE this is numerically equivalent to a long-difference regression on ΔYd vs. ΔTariffd — which is why ADH-style papers (and teaching slides) often present Bartik in differences.

Topalova: findings

- Rural districts more exposed to tariff cuts → slower decline in poverty, lower consumption growth.

- Effect concentrated among the geographically immobile and least skilled.

- Mechanism: rigid labor laws → costly to fire and to expand → factor reallocation stalls.

- In states with flexible labor regulation, the poverty effect of exposure is statistically zero.

Takeaway: Bartik captures exposure; institutions decide adjustment.

Autor, Dorn & Hanson (2013): the China shock

- Autor, Dorn, and Hanson (2013) examine US commuting zones (CZs) 1990–2007.

- China’s WTO accession (2001) and supply-side reforms drove a sustained import surge.

- Variation across CZs comes from pre-shock industry mix.

ADH: the instrument

ΔIPWcτ=∑kLck,t0Lk,t0⋅ΔMUSkτLc,t0

- Lck,t0 — start-of-period employment in CZ c, industry k

- ΔMUSkτ — change in US imports from China in industry k

To address shock endogeneity (US demand could pull in imports too), ADH instrument ΔMUS with ΔMOTH — imports from China to eight other rich countries. This isolates the China-side supply shock.

ADH: main results

- High-exposure CZs lose more manufacturing jobs.

- Wages fall, esp. among non-college workers.

- No offsetting employment gains in other sectors at the local level.

- Effects persist for at least a decade.

- Autor, Dorn, and Hanson (2016) (2016 review) extends to job churning, lifetime earnings, social spending, marriage rates, mortality.

Why ADH matters methodologically

- Cleanest example of the shock-based identification logic in BHJ.

- The “other rich countries” instrument is the canonical move for purging demand-side endogeneity from a Bartik.

- Sparked the AKM (2019) literature on inference because their headline SEs were too tight.

- Their data and Stata replication files are widely used in teaching.

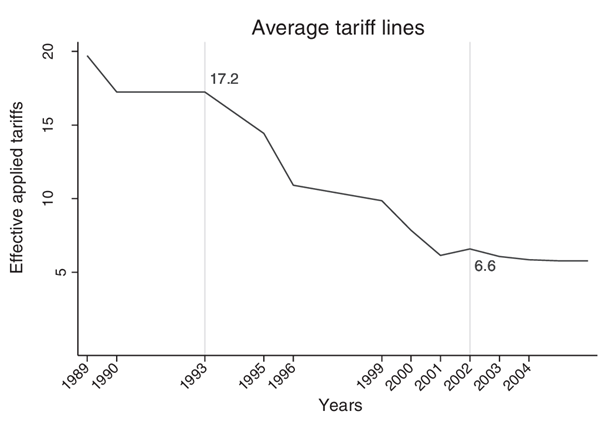

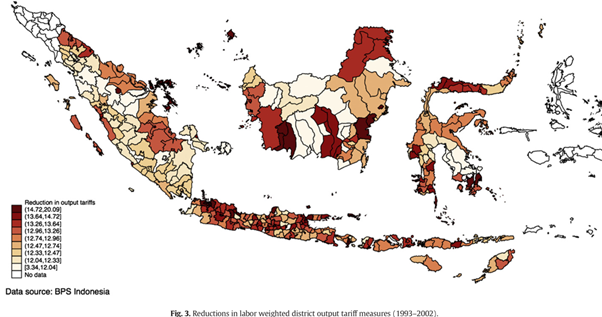

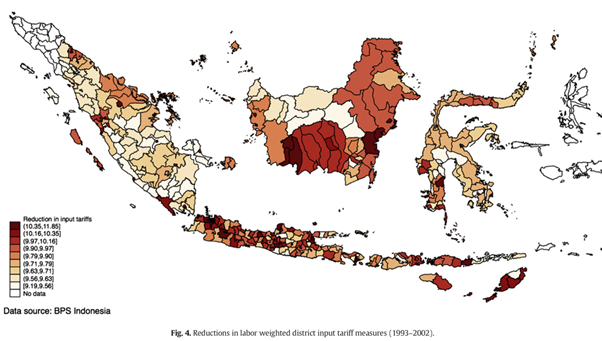

Kis-Katos & Sparrow (2015): Indonesia 1993–2002

- 259 districts; outcome is district-level poverty.

- Two waves of tariff cuts: WTO 1995 + IMF program 1999.

- Innovation: separate output and input tariff exposure using a 1990 input-output table.

Output vs. input tariffs

Otkt=S∑s=1(Qsk,t=0Qk,t=0×tst)

Itkt=S∑s=1(Qsk,t=0Qk,t=0×J∑j=1Mjs,1990Ms,1990tjt)

sector s, district k, time t, input sector j, labor Q, tariff t

The first share weights output tariffs by district industry mix; the second additionally weights through the I-O matrix to capture imported intermediate inputs embodied in each sector.

Output tariff exposure

Input tariff exposure

Kis-Katos & Sparrow: findings

Δykt=α+β1Otkt+β2Itkt+γΔX′kt+I′kθ+λrt+Δϵkt

- β1>0 — output tariff cuts raise poverty (import competition story).

- β2<0 and larger in magnitude — input tariff cuts reduce poverty (cheaper intermediates → firm competitiveness → low-skill work participation and middle-skill wages rise).

Net effect on Indonesian poverty is negative — but only because input tariff liberalization dominates. The distributional story matters.

Three applications side by side

| Topalova (2010) | ADH (2013) | KK & Sparrow (2015) | |

|---|---|---|---|

| Country | India | US | Indonesia |

| Episode | 1991 reform | 1990–2007 | 1993–2002 |

| Unit | districts | commuting zones | districts (259) |

| Shock | tariff cuts | China imports | tariff cuts (2 waves) |

| Share | 1987 employment | start-period emp. | I-O × employment |

| Outcome | poverty, consumption | jobs, wages | poverty |

| Direction | exposure ↑ → poverty ↑ | exposure ↑ → jobs ↓ | output↑ poverty↑, input↓ poverty↓ |

Hands-on with R

The dataset

dat.xlsx — 3 regions, 2 sectors, 2 years. Toy data so you can verify by hand.

# A tibble: 12 × 5

year region sector tariff labor

<dbl> <chr> <chr> <dbl> <dbl>

1 1987 A Agri 30 100

2 1987 B Agri 30 1000

3 1987 C Agri 30 700

4 1987 A Manuf 20 9000

5 1987 B Manuf 20 400

6 1987 C Manuf 20 3000

7 1988 A Agri 10 110

8 1988 B Agri 10 1100

...Step 1 — compute 1987 employment shares

Step 2 — compute national tariff shocks

Step 3 — assemble the Bartik

# A tibble: 3 × 3

region Z_log Z_lev

<chr> <dbl> <dbl>

1 A -1.38 -15.1

2 B -1.18 -18.6

3 C -1.33 -15.9Region A is most exposed in log, region B most exposed in levels — same point we made earlier, now in code.

Step 4 — the (would-be) 2SLS

With only 3 districts there’s nothing to estimate. In a real Topalova-style exercise:

For AKM-corrected SEs, use the ShiftShareSE package and pass the share matrix.

Exercise (10 min, in pairs)

Using only dat.xlsx:

- Recompute Zℓ assuming the 1988 shares (not 1987). What’s different and why?

- Now compute it using employment growth as the shift instead of tariffs. Does the ranking of regions change?

- Region A is essentially a “manufacturing town.” If we drop A, what happens to the cross-sectional variation in Z? What does that tell you about the Rotemberg-weight diagnostic in GP?

- Suppose we observed poverty rates falling by 5pp in A, 2pp in B, 4pp in C. Compute the reduced-form slope of Δpoverty on Zℓ. Interpret with care — what assumption are you making?

What to read next

- Goldsmith-Pinkham, Sorkin, and Swift (2020) — the canonical methods paper. Tables 5–6 are the diagnostic template you should copy in your own work.

- Borusyak, Hull, and Jaravel (2022) — when shocks (not shares) carry identification.

- Adão, Kolesár, and Morales (2019) — the inference paper. The R package

ShiftShareSEimplements it. - Autor, Dorn, and Hanson (2013) + Autor, Dorn, and Hanson (2016) (review) — the China shock canon.

- Topalova (2010) — the trade-and-poverty workhorse for developing countries.

- Kis-Katos and Sparrow (2015) — the closest Indonesian benchmark for your own work.

Frontier and Indonesian context

- I-O Bartik: extend KK & Sparrow’s input/output split to services value-added (GVC trade).

- Granular instruments: large firms as shock units instead of sectors (Gabaix-Koijen 2024).

- Uncertainty as a shift: ongoing work by Pane, Massie & Gupta (2025) uses a geopolitical uncertainty index in place of tariff changes — the share captures exposure to uncertain trading partners rather than to specific industries (Pane, Massie, and Gupta 2025).

- Whatever the shift, the identification logic is the same: argue for either share exogeneity or shock exogeneity, then show diagnostics consistent with that argument.

Wrap-up

- Bartik = shares × shifts → predicted regional exposure.

- Two identification stories; pick one and live by it.

- Always report Rotemberg weights or shock-balance tests.

- Use AKM SEs, not white SEs.

- The trade-policy applications (Topalova, ADH, KK & Sparrow) give you a recipe you can transplant onto any Indonesian liberalization episode.