Kajian Perekonomian Asia Tenggara

ASEAN Trade and Economic Integration

2026-04-14

Today’s agenda

Part 1: Theory of economic integration — stages, trade creation/diversion, Rules of Origin

Part 2: ASEAN integration in practice — AFTA, AEC, RCEP, GVCs, logistics

Part 3: Geopolitics and current challenges — US-China trade war, Trump tariffs, ASEAN positioning

Wrap-up: Key takeaways and discussion

Why do countries integrate?

Unilateral tariffs are individually rational but collectively harmful — a prisoner’s dilemma

Trade agreements lock in cooperative outcomes and avoid trade wars

Deeper integration reduces transaction costs beyond tariffs: standards, regulation, mobility

Political dimension: peace and stability through economic interdependence (Baldwin and Wyplosz 2020)

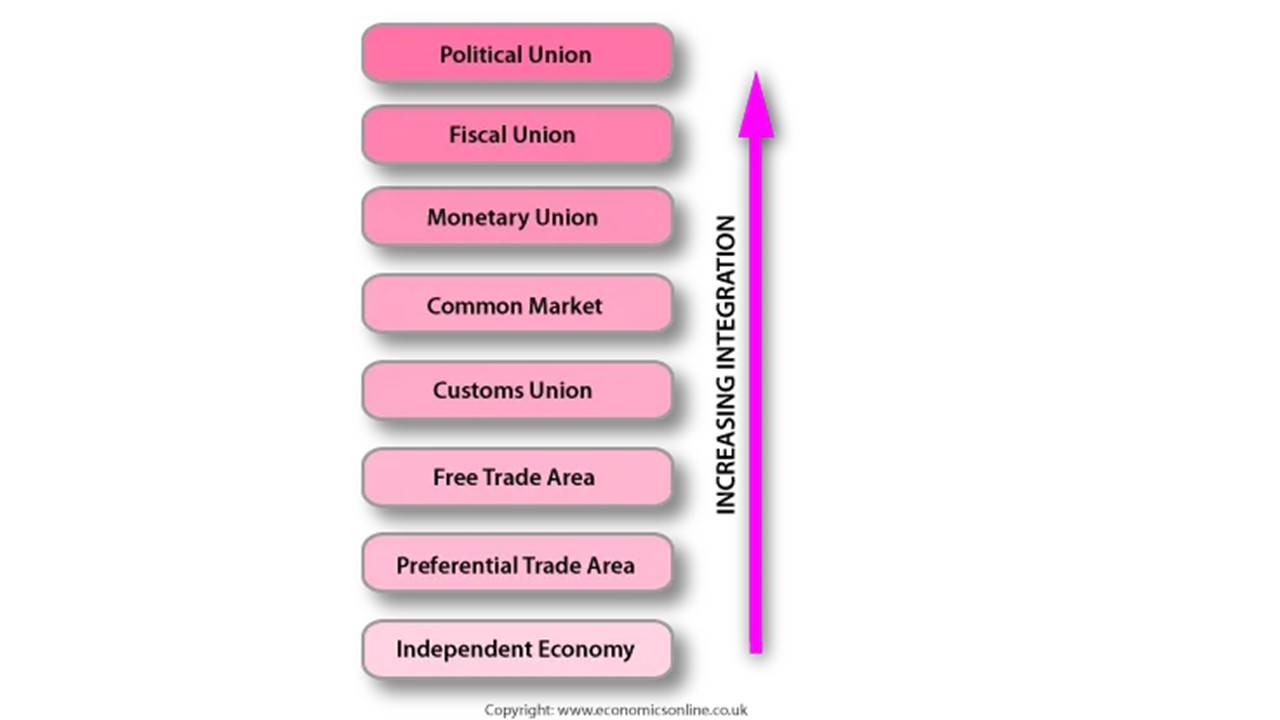

Stages of economic integration

The integration ladder

Preferential Trade Area (PTA): partial tariff reductions among members (e.g., ASEAN PTA 1977)

Free Trade Area (FTA): zero/near-zero tariffs among members, each keeps own external tariff (e.g., AFTA)

Customs Union (CU): FTA + common external tariff (e.g., EU began here in 1968)

Common Market: CU + free movement of labor and capital

Economic/Political Union: common policies, single currency, shared institutions (EU today)

Trade creation vs trade diversion

Trade creation: members switch from costly domestic production to cheaper partner imports — welfare gain

Trade diversion: members switch from efficient non-member to less efficient member — welfare loss

Net effect depends on: member efficiency, initial tariff levels, and complementarity of economies

Key question for ASEAN: are member economies complements or substitutes? (Verico 2022; Widyasanti 2010)

Rules of Origin (ROO)

In an FTA (no common external tariff), ROO prevent “tariff shopping” via the lowest-tariff member

Types: value-added threshold, change in tariff classification, specific process rules

Complex ROO increase compliance costs — act as a hidden trade barrier

ASEAN’s ROO historically fragmented across multiple ASEAN+1 agreements

This fragmentation is called the “noodle bowl” of overlapping FTAs (Widyasanti 2010)

The EU benchmark

EU achieved >60% intra-regional trade share

Customs union since 1968, single market since 1993, single currency (euro) since 1999

Supranational institutions enforce compliance (European Commission, ECJ)

“The ASEAN way” (cara ASEAN) is deliberately different: consensus, non-interference, sovereignty retained (Baldwin and Wyplosz 2020; Ishikawa 2021)

Discussion

Can ASEAN ever achieve EU-level integration? What are the main obstacles?

Think about: political systems, income gaps across members, cultural diversity, sovereignty preferences

Key insight: ASEAN chose flexibility over depth — is that a feature or a bug?

ASEAN Integration in Practice

ASEAN’s integration journey

1967: ASEAN founded — political and security cooperation

1977: ASEAN PTA — first trade preferences among members

1992: AFTA signed — target 0-5% tariffs by 2010 (ASEAN-6) / 2015 (CLMV)

2007: AEC Blueprint — beyond tariffs: services, investment, skilled labor, capital flows

2015: AEC formally launched (but implementation incomplete)

2022: RCEP enters into force — ASEAN + China, Japan, Korea, Australia, New Zealand (Ishikawa 2021; Daniswara and Revindo 2022)

Shallow integration

Intra-ASEAN trade: ~22-23% of total — stagnant for two decades

Compare: intra-EU trade >60%, intra-NAFTA/USMCA ~40%

Extra-ASEAN trade is growing fast, so absolute intra-ASEAN trade grows too — but the share does not

AEC achieved tariff elimination but not deeper integration (Daniswara and Revindo 2022; Revindo 2019)

Why “shallow integration”?

Three key structural reasons:

Substitutes, not complements: ASEAN members export similar goods (palm oil, rubber, electronics assembly) — limited gains from trading with each other

NTMs and complex ROO: non-tariff measures proliferating even as tariffs approach zero; fragmented ASEAN+1 ROO regimes (the “noodle bowl”)

Heavy reliance on CJK: China, Japan, and Korea provide technology, capital goods, and scale — ASEAN integrates more with them than with each other (Verico 2022; Widyasanti 2010)

Logistics: the hidden barrier

Logistics costs in ASEAN remain high and uneven across members

Port infrastructure gaps, especially in CLMV countries (Cambodia, Laos, Myanmar, Vietnam)

Customs procedures and documentation remain complex despite the ASEAN Single Window initiative

Logistics performance strongly predicts bilateral trade flows within ASEAN

Indonesia’s archipelago geography adds unique cost challenges (Ardine and Revindo 2023)

GVC participation and the unbundling framework

Kimura’s 3 unbundlings: (1) production from consumption, (2) tasks from firms, (3) people from tasks via digital technology

ASEAN’s strength: the 2nd unbundling — fragmented manufacturing across borders (electronics, automotive)

But ASEAN is mostly in low-value assembly segments; moving up requires services and technology capabilities

The 3rd unbundling (digital services trade) is the new frontier for ASEAN (Kimura 2018; Revindo 2024)

Supply chain resilience

COVID-19 and US-China tensions exposed concentration risk in global supply chains

Import source diversification improves resilience to supply shocks

ASEAN countries with more diversified import sources recovered faster from disruptions

Policy implication: regional integration (especially RCEP) can help diversify away from single-source dependency (Ar-rafif and Revindo 2025)

RCEP: a game changer?

RCEP unifies ASEAN+1 FTAs into one framework (ASEAN + China, Japan, Korea, Australia, New Zealand)

Key innovation: cumulative Rules of Origin — all 15 members count as “one source region”

Also covers: investment, services trade, e-commerce, intellectual property

Tariff impact modest (most tariffs already low) — but ROO simplification and NTM harmonization are significant

India opted out — implications for supply chain diversification strategy (Daniswara and Revindo 2022; Revindo 2019)

Quick quiz

Why is intra-ASEAN trade share stagnant at ~22% despite tariffs approaching zero?

Hint: think beyond tariffs — what are NTMs? Why does the substitutes-not-complements problem matter?

Follow-up: how might RCEP’s cumulative ROO change the picture?

Geopolitics and Current Challenges

The US-China tariff war

Trade war escalated from 2018: tariffs imposed on ~$550 billion of bilateral trade

Direct effect: trade diversion benefits some ASEAN members (Vietnam, Malaysia)

Indirect effect: uncertainty reduces investment; supply chain restructuring is costly and slow

Net effect on ASEAN: mixed — short-term trade gains but long-term strategic risk (Riefky, Sabrina, and Revindo 2025)

Trade redirection: who benefits?

Vietnam: largest beneficiary — FDI surge, export growth to US markets

Malaysia, Thailand: electronics and auto parts reshoring from China

Indonesia: some gains in textiles and metals, but held back by logistics costs and regulatory barriers

Risk: “transshipment” scrutiny — the US is investigating Chinese goods rerouted through ASEAN members (Riefky, Sabrina, and Revindo 2025)

“Bebas aktif” (independent and active)

Indonesia’s foreign policy doctrine: independent and active — bebas aktif

ASEAN consensus: stay neutral, engage both powers, avoid bloc alignment

“Playing both sides” (main dua kaki) to maximize economic benefit

ISEAS 2024 survey: 50.5% of ASEAN respondents would choose China over the US if forced to pick — trend shifting toward China

But forced alignment remains unlikely; ASEAN’s value is precisely its neutrality

Competing frameworks

RCEP (2022): comprehensive, binding, includes China — trade + investment + services

IPEF (2021): US-led, no market access commitments, pillar-based (supply chains, clean economy, tax, anti-corruption) — status uncertain under Trump 2.0

Bilateral FTAs: Indonesia-UAE CEPA (2024), Indonesia-EU CEPA (ongoing negotiations)

Key tension: RCEP deepens integration with China; IPEF offers no tariff reductions; bilateral deals are piecemeal (Revindo 2019; Ishikawa 2021)

Free Trade Zones / KEK (Kawasan Ekonomi Khusus)

FTZs offer tariff and regulatory exemptions in designated areas to attract FDI

Case study: Oecusse-Ambeno (Timor-Leste) — FTZ impact on local economic growth

ASEAN examples: Batam (Indonesia), Iskandar (Malaysia), various SEZs across the region

Can bypass national-level integration barriers — but risk a “race to the bottom” on regulation (Shaohong and Revindo 2024)

2026 context

Trump’s “Liberation Day” tariffs (April 2025): broad reciprocal tariffs on ASEAN members

Indonesia hit with 32% tariff (among the highest); Vietnam 46%, Thailand 36%

ASEAN response: negotiation, not retaliation — bebas aktif (independent and active) in action

Trade redirection accelerating: Chinese firms setting up operations in ASEAN to circumvent US tariffs

Indonesia’s opportunity: attract manufacturing — but requires regulatory reform, logistics investment, and human capital upgrading

Discussion

Is ASEAN’s neutrality sustainable in an increasingly polarized world?

Should Indonesia prioritize RCEP deepening, bilateral FTAs, or domestic reform?

What would “forced to choose” look like in practice — and what would it cost?

Key takeaways

ASEAN chose shallow, flexible integration — “the ASEAN way” — a deliberate trade-off against EU-style depth

Tariffs are mostly gone; the real barriers are NTMs, logistics, ROO complexity, and structural similarity among members

RCEP is the most significant recent development — cumulative ROO could be transformative

Geopolitical competition (US-China) creates both risks and opportunities for ASEAN

Indonesia must invest in logistics, regulatory reform, and GVC upgrading to capture these gains

Questions for next week

How can ASEAN move from “shallow” to “deep” integration without becoming the EU?

What is the optimal trade strategy for Indonesia in the current geopolitical environment?

Can digital trade (the 3rd unbundling) help ASEAN leapfrog traditional integration barriers?

Reading list

- Baldwin and Wyplosz (2020) — Ch. 1-3 (integration theory)

- Verico (2022) — ASEAN integration principles

- Kimura (2018) — unbundlings and development strategies

- Ardine and Revindo (2023) — logistics and intra-ASEAN trade

- Riefky, Sabrina, and Revindo (2025) — US-China tariff war impact

- Ar-rafif and Revindo (2025) — import diversification and supply chain resilience